PR1MA launched SPEF (Skim Pembiayaan Fleksibel/Flexible Financing Scheme) with the hope to increase loan approval for PR1MA house buyer. It is understood that many qualified purchasers of PR1MA scheme are unable to secure a housing loan, hence could not own their home even with PR1MA. How does SPEF actually work?

How does SPEF works?

First of all, it allows only paying interests for the first 5 years. Is this something special? This is actually as any of our property bought from developer. During construction period, most borrowers are paying only interest during the period of time based on amount drawn down by developers. In this case SPEF could be viewed as extra 2-3 years extension of interest paying only as currently our standard construction period is 2 years for landed and 3 years for high rise residential.

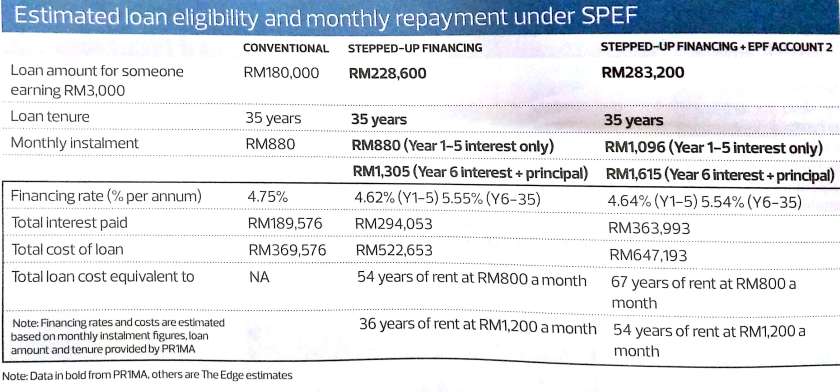

By paying interest only during the first 5 years means if you are serving 35 years loan, your 35 years begin when you start to pay full instalment (the 6th year). Further to that, you are paying highest amount of interest during the first 5 years since no reduce in principal amount. The cost impact is illustrated by The Edge Malaysia as below.

*Source : The Edge Malaysia, 20th-26th Feb 2017, page 8, “Housing loans are not always productive debt”

*Source : The Edge Malaysia, 20th-26th Feb 2017, page 8, “Housing loans are not always productive debt”

How does SPEF increase the chance of approval for Housing Loan?

As known to most of us, Debt Service Ratio (DSR) is one of the major consideration in housing loan approval especially in determining the amount of loan eligible. Most of the banks allow DSR ratio up to 70% or 85%. Therefore, an increase or RM 100 a month in repayment ability could actually increase about RM 20,000 in loan amount. SPEF Step Up allows borrowers to justify repayment by taking into consideration monthly EPF contribution by both employer & employee into EPF Account 2. Using example below, referring to RM 216 of example one is derived from 30% of (RM 3000 x 24% (11% employee + 13% employer). By additional amount of RM 216, one could actually arrives at extra loan amount of near to RM 45000 (total loan – approx. RM 232,300). This is considered as level one step up loan under SPEF.

Example below is illustration of Step Up Level 2 as borrowers would also agree to use the accumulated amount in account 2 of EPF to pay instalment. (for the terms & condition, kindly refer to www.pr1ma.my) In this illustration, it is assumed that loan amount eligibility is based on instalment ability of borrowers in the first 5 years which is paying interest only. (RM 283,300 x 4.75%/12 = RM 1121). However, we have doubt over this assumption as banks would need to determine further how much amount has actually been accumulated in EPF Account 2, many might not have accumulated a lot, especially those looking for first house might comprised of many who has just started work for not long ago.

As of this time of this article, we have yet to gather enough information from participating banks (Maybank, CIMB, RHB & Ambank) in regards to this matter.

*Source : The Edge Malaysia, 20th-26th Feb 2017, page 8, “Housing loans are not always productive debt”

Points to consider for PR1MA buyer?

- EPF always allow members to withdraw amount from EPF Acc 2 as down payment for purchasing first house. Should you have sufficient amount in Acc 2, you may consider to make EPF withdrawal and pay higher down payment, which resulting lower loan amount, hence, lower monthly instalment and subsequently lower DSR. Many may not be aware that, one is allowed to withdraw a total amount (Property Price – Loan Amount) + 10%. This means that you can actually withdraw 30% of property price from EPF account 2 if you are taking only 80% loan.

- Have you done your credit management? The extra repayment ability by taking EPF monthly contribution as discussed above can easily being cancelled off by your other loan commitment. For example, an outstanding amount of RM 3000 in your credit card account would have been considered as RM 150 monthly expenses. Or you might have a personal loan / hire purchase loan that is about to complete in few months time. We would advise you to talk to a mortgage advisor to understand you own situation prior to make any decision.

- Are you ready to utilise your retirement fund for owning your house? Typically Malaysian doesn’t save enough for retirement. By fully utilising EPF Account 2 might further reduce our saving for retirement. Further to that, we can not do any other withdrawal even for Medical in the event of emergency until the loan is fully paid up.